The September Detroit Metro Real Estate market continued to follow the same post tax credit pattern with continued falling available home inventories and a relatively strong sales pace. In terms of historical numbers, sales dropped compared to 2009, but remember 2009 was getting near peak tax credit activity, so even coming close is good. The more relevant comparison is pre tax credit 2008, which we were ahead of. Available home inventories for the Metro Detroit market remain at a 3 year low, another good sign. The rest of the state has not yet seen the same declines but their inventories did not rise as high either. In general, the Southeast Michigan market is the healthiest in the state and one of the most active in the country. The rest of the state should follow, since most depend on SE Michigan to some degree.

Foreclosure moratoriums by many of the major banks have been the hottest industry news. Below is a good article that explains what is going on and how it happened. In general, the major banks have found enough issues with their foreclosure process that they have stopped taking possession of homes and in many cases are taking their homes off the market. It is too early to tell if this is a 30 day or 6 month issue. Their action will further shrink the available housing inventory so it may have a short term positive market effect, but the reality is the sooner the bank inventories are moved through the market, the faster we will get to a permanent improving market.

With fewer bank owned homes on the market to compete with, the moratorium does offer a short term opportunity for sellers to get a value boost (not so much appreciation, but a price a bit closer to typical asking prices) by putting their homes on the market now.

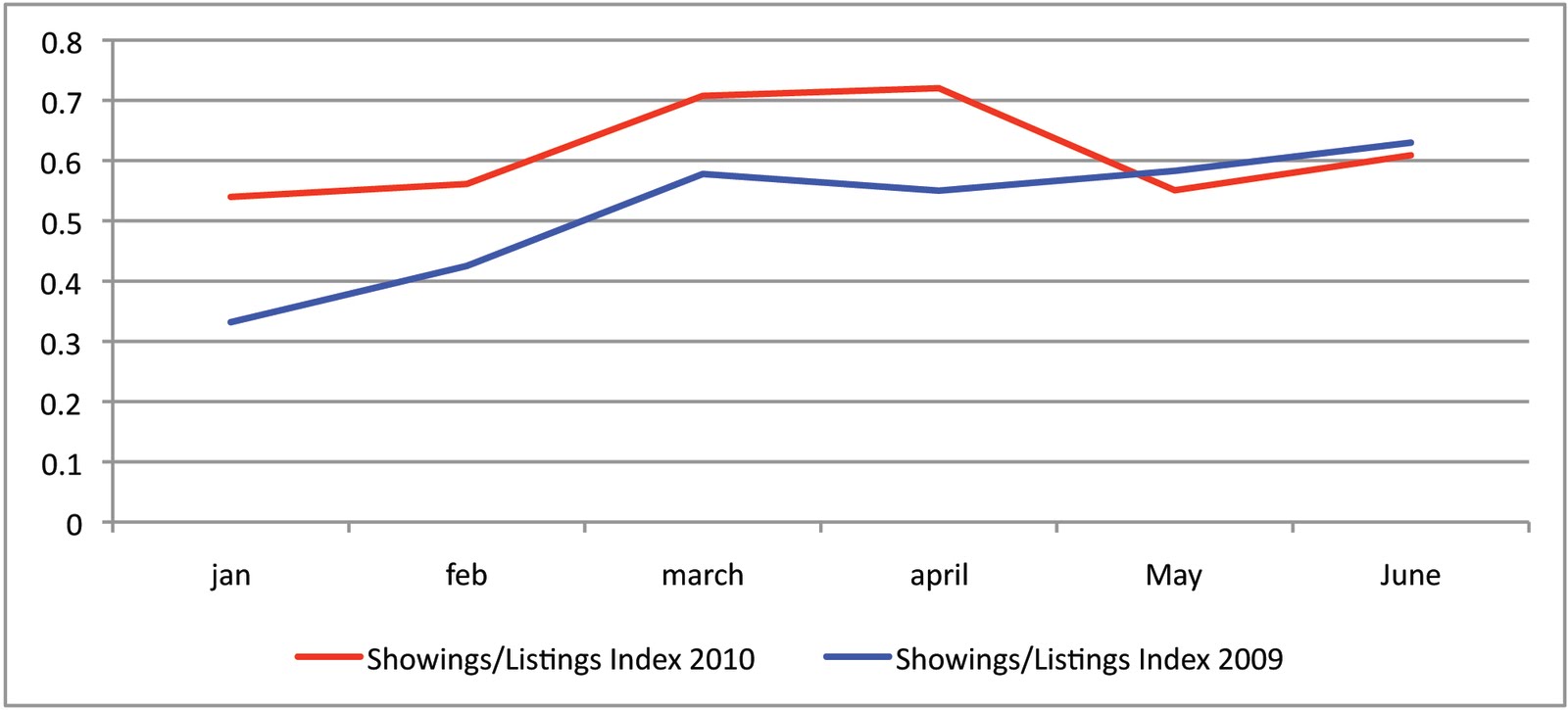

The chart below puts the current sale pace in historical perspective. The last few months have been at a pace closer to 2005/06, quite a bit ahead of the low points in 2007/08.

Also, here is a chart of the average price per square foot for SE Michigan sold properties (Excluding the City of Detroit). You can see the effect even a short-term reduction in supply can have on value with the rise in prices during the tax credits.

_________________________________________________

A Primer On The Foreclosure CrisisJOHN CARNEY, CNBC, CADIE THOMPSON, NETNET, NET NET, FORECLOSURES, REAL ESTATE, HOUSING, FORECLOSURE, BANK OF AMERICA, JPMORGAN

Posted By: John Carney | Senior Editor, CNBC.com

CNBC.com

| 11 Oct 2010 | 02:48 PM ETLast week,

Bank of America announced that it was halting foreclosures in all fifty-states while it reviewed its foreclosure process for defects. Now several lawmakers on Capitol Hill are calling for other banks to initiate nationwide foreclosure freezes—a move which the Obama administration is currently opposing.

So what’s going on here? Why is the foreclosure machinery of our nation’s largest banks suddenly grinding to a halt? What does this mean for the financial sector and the economy?

Let’s start with the most basic questions first. Then I’ll explain some of the possible implications for homeowners, banks, and the economy.

How did this thing get started?Ever since the housing bubble burst, there have been signs that there are serious problems with foreclosure practices. In some cases, the financial institution claiming it owns the mortgage has not been able to produce the underlying loan documents. In 2007, a federal judge held that Deutsche Bank lacked standing to foreclose in 14 cases because it could not produce the documents proving that it had been assigned the rights in the mortgages when they were securitized.

This decision was followed by similar rulings in other states stopping foreclosure proceedings. Typically the judges would find that the banks that were servicing mortgages pooled into bonds weren’t able to prove they owned the mortgages.

Why can’t they prove they own the mortgages?Every time a mortgages changes hands, the new owners are supposed to receive an “assignment” of the mortgage notes from the buyers. The assignment is typically a short little document signed by both the seller and buyer of the mortgage acknowledging the sale, which is then attached to the mortgage documents themselves and delivered to the new owner.

When a mortgage is securitized it is typically sold to a Wall Street firm, which pools the mortgage with thousands of others. Investors buy slices of the pool, entitling them to cash-flows from the mortgage payments. The actual mortgages are assigned to a newly created investment vehicle. A servicer is tasked with ensuring the payments to borrowers get divided up properly and that delinquent borrowers get foreclosed upon.

Here’s where things get tricky. When a mortgage is securitized, the investors in the mortgage bonds don’t get assignments or notes. The investment vehicle doesn’t get the assignments or notes either. Instead, the physical notes are typically sent to a document repository company. The transfer of interests is noted in an electronic database.

But during the height of the housing bubble, investment banks were churning out mortgage bonds in such a frenzy, sometimes the assignments never got executed and mortgage notes never got delivered. Keep in mind that this was during the years when lenders were giving out low-doc and no-doc mortgages. It was inevitable that the fast and loose and slightly documented culture would not stop at the mortgage originator but stretch all the way through the process. (For more on this, see RortyBomb’s excellent discussion of the securitization process, complete with nifty and highly informative charts.)

For most mortgages, the note probably still exists somewhere. One problem that has arisen, however, is that some of the original mortgage lenders have gone under or been acquired by a larger bank. This can make tracking down the notes difficult, if not impossible.

Why am I just learning about this mess now?This issue has been quietly simmering in the background of the housing crisis for quite some time. Gretchen Mortgenson of the New York Times wrote about it back in 2007. It gave rise to a “show me the note” movement of people contesting foreclosure proceedings.

But what really kicked off the latest developments was the deposition of a GMAC loan officer named Jeffrey Stephan, which revealed deep and perhaps pervasive flaws in the foreclosure practices of our largest banks.

Stephan admitted in a sworn deposition in Pennsylvania that he signed off on up to 10,000 foreclosure documents a month for five years. He said that he hadn’t reviewed the mortgage or foreclosure documents thoroughly. He quickly became known by the pejorative “robo-signer” for this way of getting mortgages through. This prompted Ally, which owns the GMAC mortgage company, to halt foreclosures in 23 so-called “judicial states.”

Because Stephan also signed foreclosures for hundreds of other mortgage companies, including J.P. Morgan Chase , the problem is not limited to GMAC. In fact, JP Morgan Chase also halted foreclosures in the judicial states.

Wait, what’s this about judicial states?The majority of states in the country allow banks to foreclose on defaulted mortgages without going to court. They simply deliver the borrower a notice of the foreclosure sale. This is the method of foreclosure preferred by banks, since it is much faster and easier to execute the foreclosure sale, and much more difficult for borrowers to contest.

Twenty-three states, however, require banks to go to court to get a foreclosure order. These are the “judicial states.” In these states, banks are typically required to produce a sworn and notarized affidavit of a loan officer and submit the mortgage documents. Often, however, judges will issue foreclosure orders without the mortgage documents so long as the borrower doesn’t contest this point.

Keep in mind that in both judicial and non-judicial states, there are strong legal presumptions that favor the banks. So long as they have the mortgage note and the loan is delinquent—or so long as no one argues that they aren’t the owners of the mortgage or that borrower is not in default—the bank will almost always get the foreclosure.

But as the “show me the note” movement took off, more and more homeowners began to contest foreclosures by demanding to see the notes and, if the loan had been transferred or securitized, the assignment agreements. This typically was not fatal to banks seeking foreclosures. They could make up for the lost notes with lost note affidavits and retro-actively build an assignment chain. The worst that would happen, from the bank’s perspective, was that the foreclosure would be delayed.

In some cases, however, banks seem to have not even been able to manage even this kind of corrective action. Evidence has been produced to show that notarizations have been faked, documents forged, and folks like Stephan have simply been operating as foreclosure bots.

So is this just a concern for “judicial states?”Although banks first shut down foreclosures in judicial states, the lack of documentation is a problem in any jurisdiction. Homeowners contesting foreclosures in both non-judicial and judicial states can win if the bank cannot provide documents proving it owns the mortgage.

In judicial states, however, the banks are especially exposed because they must initiate a lawsuit to get a foreclosure. If they have been submitting false documents to the court, they could be sanctioned and fined. Realizing that they had few internal controls over their own foreclosure practices, banks wisely shut down foreclosures in the states where they had the most exposure.

In non-judicial states, banks aren’t required to submit anything to the court until they are sued by a homeowner seeking to stop a foreclosure. That means that they are far less likely to submit fraudulent documents, since the process has already been slowed. Nonetheless, banks may still find themselves swamped by challenges. No one really knows how badly the missing documentation problem is at the banks.

The Wall Street Journal told me this is just about “paperwork” and politics. Are we making a mountain out of a molehill?Our friends at the Journal are seriously misguided on this issue. (Note: my brother, Brian Carney, is on the editorial board of the Journal.)

The requirement that banks be able to prove ownership of mortgages by producing notes and assignments reflects a long-settled view about the necessity of written contracts in real estate transactions. Long before the founding of our Republic, England adopted what is commonly called the “Statute of Frauds.” It required that real estate conveyances be recorded in writing and signed. Similar laws apply in almost every state in the Union.

Part of the point of the writing requirement is to allow the government the transparency it needs to enforce property rights, including the right to foreclose on a home. If courts were to treat this as mere “paperwork” that was irrelevant to the cases, both property rights and the rule-of-law would suffer. It’s surprising that the Journal’s editorial page would take this stance.

Now, if the problem truly is just sloppy work on the part of robo-signers, banks can likely resume foreclosures before too long. But many suspect that the reason banks were falsifying their knowledge about the possession of loan documents is that the banks do not actually have the documents and don’t know where to find them. This could permanently impair their ability to foreclose on some properties.

What does this mean for the banks?In the first place, the slowdown in foreclosure sales might hit the revenues of the banks. The defaulted loans aren’t spinning off revenue and now the foreclosures aren’t producing revenue either. If the foreclosure freezes last long enough, this could it the bottom lines of the banks. At the very least, banks should be adjusting the estimates on the likelihood of short-term recovery values for their mortgage portfolios.

The fact that banks securitized loans but did not get proper assignments of the mortgage notes may find themselves liable to lawsuits from investors. A typical mortgage bond issuance includes representations and warranties that all the proper documentation has been obtained. Banks could find themselves liable for a breach of these warranties.

This could also turn into a fight between investors of junior and senior tranches of mortgage bonds. Here’s how the

Journal describes this fight:

When houses that have been packaged into a mortgage bond are liquidated at a foreclosure sale—the very end of the foreclosure process—the holders of the junior, or riskiest debt, would be the first investors to take losses. But if a foreclosure is delayed, the servicer must typically keep advancing payments that will go to all bondholders, including the junior debt holders, even though the home loan itself is producing no revenue stream. The latest events thus set up an odd circumstance where junior bondholders—typically at the bottom of the credit structure—could actually end up better off than they expected. Senior bondholders, typically at the top, could end up worse off. Not surprisingly, senior debt holders want banks to foreclose faster to reduce expenses. Junior bondholders are generally happy to stretch things out. What is more, it isn't entirely clear how the costs of re-processing tens of thousands of mortgages will be allocated. Those costs could be "significant" said Andrew Sandler, a Washington, D.C., attorney who represents mortgage companies.The most damaging thing that could happen to banks would be the discovery that they simply cannot prove they hold a mortgage on a house. In that case, the loan would probably have to be written down to near zero. Even for current loans, the regulatory reserve requirements would double as the loan would no longer be a functional mortgage but an ordinary consumer loan. Depending on the size of the “no docs” portion of the loan portfolio, this might be a minor blip or require a bank to raise new capital to fill the hole in the balance sheet.

What does this mean for the housing market and the economy?Get ready to hear the phrase “pig through the python” a lot. For example, “We need to get the pig through the python very quickly so that the market can be free of uncertainty.”

This is the favorite metaphor of bankers discussing the foreclosure crisis. The idea is that anything that slows down foreclosures will unsteady the housing market. There’s a lot of truth to this. Buyers will hesitate to bid on foreclosure sales if they are not confident the foreclosure is legitimate. Other buyers may worry that the lack of foreclosure sales in an area is a false indicator of the health of the local housing market.

Banks concerned about the recovery values of their mortgage portfolios and higher capital requirements, may pull back lending even further than they already have. In short, this could be the beginning of the second leg of the credit crunch.